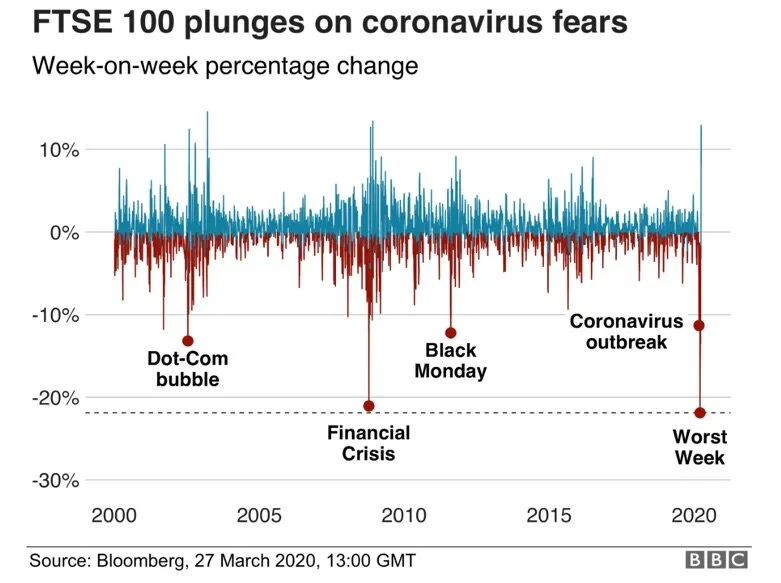

The start of a new decade sparked hope that something good was coming. 2020 started off seemingly normal for most people: celebrating New Year’s, making strides towards their resolutions, and going about their normal lives as they had done in 2019. That is until COVID-19, also known as the coronavirus, tilted the world on its axis. Even though the coronavirus approached the United States slowly, it hit hard. The effects have been felt in all aspects of people’s lives: the country went on lockdown, once-booming businesses permanently closed their doors, and the economy grinded to a halt; indeed, COVID-19 is the biggest economic crisis since the Great Recession nearly a decade ago.

The tagline that reverberated throughout the country on the cause of the Great Recession was that “the housing bubble had burst”. Underneath that tagline laid a complex world of questionable banking practices—approving huge mortgage amounts for borrowers knowing that borrowers could never pay back those loans and not keeping enough funds in the “rainy day” funds for when banks themselves would face severe financial issues. These risky practices by big players in the financial world eventually led to an economic meltdown. In the end, the federal government rescued banks by throwing them a lifeline worth billions of dollars.

Fast forward to 2020 and once again borrowers are backing out of mortgage agreements and missing their mortgage payments because of substantial job losses resulting from the pandemic. With the country’s economy now essentially paralyzed by the pandemic, the question is whether the federal government will once again put on its cape and come to the rescue. Congress has already passed a $350 billion bailout program to help businesses and is currently negotiating a second round of additional funds.

What’s important to remember from 2008 is that on top of the billions of dollars used, Congress also adopted the most substantial financial reform laws since the Great Depression of the 1930s: the Dodd-Frank Act. Dodd-Frank improved accountability in the financial system through strict financial regulations on banks such as the annual stress tests. Created by the Federal Reserve Bank, these tests are stressful hypothetical economic scenarios and the goal of the tests is to determine if each regulated banking entity would have enough in their “rainy day” funds to survive another financial crisis. To use the analogy of a law school student, the stress tests are akin to a difficult three-hour law school final exam where students have to apply their knowledge from hundreds of pages worth of reading to hypothetical fact patterns. The hope is that banks (and law students) will survive the pressure. The real benefits of annual stress tests on banks (perhaps less so on law students) are: (1) aiding banks in knowing how much money is enough to function properly even under the worst economic fluctuations, and (2) providing valuable systemic information on how theoretical financial shocks would affect different sized banks collectively and individually.

Despite these benefits, President Trump got rid of stress tests by enacting a new deregulatory measure in 2018. Conservatives had criticized the stress tests for placing unreasonable burdens on banks and highlighted how much money each bank had to spend to conduct them. For example, Citigroup, a banking giant with nearly $20 billion in profits in 2019, spent $180 million in 2015 to hire outside consulting firms to advise them on how to alter their banking practices to pass the stress tests for the year. Of course, Citigroup had to spend this $180 million because of its own inaction to ensure sufficient assets were in the rainy day funds to pass the stress tests initially conducted by the Federal Reserve in 2015. Even so, $180 million is admittedly a large amount of money to pass a hypothetical test for a single year.

The answer though is not to abandon stress tests altogether; if anything, the current coronavirus pandemic proves that we must continue to test the health of our financial institutions to ensure that our economy can withstand what inevitably will be future crises. Crisis can originate from the most unexpected sources. For instance, the housing bubble was man-made but the coronavirus demonstrates financial collapse can also come from natural phenomena.

Let’s return to stress tests. I propose a new top-down model of stress testing for banking entities that were foolishly removed from the oversight of the Federal Reserve through Trump’s 2018 reversal. What would be new and a departure from the original Dodd-Frank Act would be the following: (1) banks should conduct stress tests on their own (as opposed to being orchestrated by the Federal Reserve), (2) the reporting of data highlighting bank-specific risks which allows the government to impose tailored supervision on individual banks, and (3) the amalgamation of test results to reveal systemic weaknesses and to provide data to help improve stress testing hypotheticals for the future. This revised model is especially workable for smaller banks with assets ranging from $50 billion to $100 billion because self-administered stress tests are more flexible and more cost effective. Requiring banks to report their test results and findings to the Federal Reserve for review, and providing public access to the data to allow for more research into how banks flourish while also being prepared for future financial disasters will be tremendous societal benefits. This new top-down model can even be expanded to include natural and social scenarios like the coronavirus pandemic which is taking the national and global economies by storm.

The Great Recession is so last decade, right? Out of sight, out of mind. But the 2018 Trump reversal of Dodd-Frank and stress tests was such a mistake and we are now faced with a public health nightmare leading us into the next full-fledged global recession. We weren’t ready for the coronavirus and neither was the economy. COVID-19 is an undeniable reminder that the next financial crisis can happen at any time for any reason, and we must stay vigilant and ready to weather it.